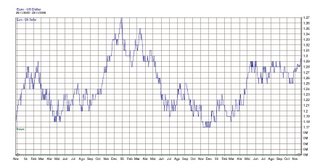

Gone are the days when our esteemed and never well weighted Euro traded below the psychological barrier of 1 USD / EUR.

The truth is that since the end of 2002 surpassed the psychological barrier, our Euro has been thrown into the bush and how! Reached the end of 2004 reaching a record high of 1.37 USD / EUR. During last year we had a period of relief, when the Euro depreciated, but this year 2006 we again placed in the orbit of 1.30 USD / EUR.

Clearly the fact that the Euro has appreciated by 9.32% so far this year has helped cushion the impact of rising oil prices and, therefore has helped contain inflationary pressures.

But what about the Euro area exports? bad business to our foreign trade (and interior) , as the appreciation of the Euro stops our exports (and imports easier.) Because of the appreciation of the Euro our goods and services abroad are more expensive (you have to deliver more USD in exchange of goods and services produced in EUR) and imported goods and services we are cheaper (you have to deliver at least EUR in exchange for goods and services produced in USD).

In other words, goods and services produced within the Euro zone have poor marketing (both domestic and export) due to loss of competitiveness caused by the appreciation of our currency. This is a torpedo at the waterline of our productive economy.

Meanwhile, the objective of price stability European Central Bank takes us in the past year have occurred five interest rate rises (presumably there will be a sixth) to stand at 3 , 25% after two and a half years of being set at 2%.

How

these increases affect us guys? First, a rise in interest rates has as its primary objective of price stability, ie keep inflation within certain levels. But as with any decision there are some side effects. Regardless of the effect, more or less immediate than on the cost of mortgages are, there is another side effect, the appreciation of the EUR against the USD.

However, in this case, the interest rate increases do not explain the appreciation of the EUR against the USD, because, although the official rate of EUR has risen 1.25% in the last year the Federal Funds Rate (the official interest rate of USD) has continued the trend that began in mid-2004 (then the official interest rate was USD 1%) and grown in the last year stood at 1.25% to 5.25%.

In fact, there is rising interest rates is explained by the appreciation of a currency, but the reduction (or expansion, as appropriate) rate differential with respect to the currency you are comparing and in this case, the past year there has been no change in the differential rate of EUR against the USD . The higher the interest rate of EUR against the USD higher the attraction to investors that currency (higher EUR demand and therefore a higher price of this coin).

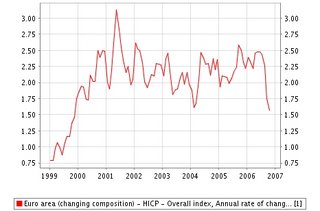

said all this, you must justify rate hikes in the euro zone, inflationary pressures do they exist to justify the increases? In principle, the escalation of oil prices presaged so, but annual rate of change of prices in the euro area in October (1.6%) is the lowest since November 1999 . The rate increase has more than fulfilled its objective, the oil starts to release pressure from speculators on demand (Ah, but they were not Chinese?), Is not the time to relax a bit and further our competitiveness?

{kind=link}